I am not writing about anything new. My concern involves an age-old (no pun intended) problem plaguing women who don’t work outside the home. It is a looming concern regarding my husband’s and my financial security as we reach old age.At least at the moment, we are together and neither of us is 100% disabled. Nevertheless, if only one of us became disabled, we would really struggle financially, while waiting 6-36 plus months to hopefully win a disability case. In addition, my husband took early retirement, which isn’t unusual for people his age. In our case, his early retirement is just shy of my monthly take-home pay. This is not surprising given the discrepancy in pay between men and women, which also affects retirement benefits. This pay inequality also extends to to career types. For example, if if you work in the upper levels of management, you are well-paid. But if you provide care for the elderly, mental health treatment, affordable housing, education , and so on, you are less likely to make a living wage. Right now, for example, there is a shortage of caregivers. Why? The wage is low, the benefits non-existent.

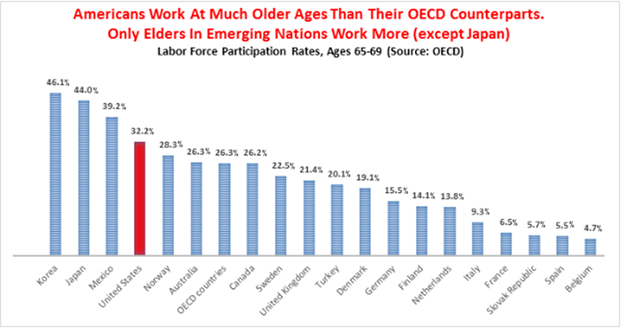

Seniors who work to supplement their Social Security (32.2%) typically earn less than $15 per hour. While encouraged to wait until age 70 to collect a higher rate of Social Security, most collect prior to that age, or even prior to the age of 65. These facts are striking because, for one of the richest nations in the world, we tolerate one of the highest poverty rates among the elderly in the highest rates in the world. Given gender-based pay inequality, this also translates to higher levels of poverty among senior women.

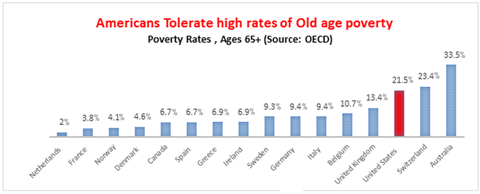

There are two ways that poverty among the elderly is calculated. One is called the “Official Poverty Measure,” which puts the poverty threshold at $11,756 a year. The other is the “Supplemental Poverty Measure,” which takes into account the taxes clients must pay, out of pocket medical expenses, homeownership, geographic area, food stamps or in-kind benefits, resources, and liabilities. I don’t know about you, but I couldn’t live on $11,756 a year. The annual rent alone in the Denver metro area, where I live, runs higher than that. Teresa Ghilarducci, in a 2018 article for Forbes, reports that,next to Australia (33.5% elderly poverty) and Switzerland (at 23.4%), the US tolerates a 21.5% elderly poverty level.

Consider the statistics on worker ages and savings presented by Ghilarducci.

According to the National Center on Aging:

· “21% of married Social Security recipients and 43% of single recipients aged 65+ depend on Social Security for 90% or more of their income. (Social Security Administration [SSA], 2016)”

· The 2.1 million older adults on Supplemental Security Income (SSI) receive, on average, just $435 each month. (SSA, 2016)

· On average, older women received about $4,500 less annually in Social Security benefits in 2014 than older men due to lower lifetime earnings, time taken off for caregiving, occupational segregation into lower wage work, and other issues. Older women of color fare even worse. (SSA, 2015)

· Nearly half a million older adults aged 55-64, and 168,000 aged 65+ who wanted to work were unemployed 27 weeks or longer in 2014. (Bureau of Labor Statistics [BLS], 2015)

· Older workers of color are most at risk for unemployment, with older African American men twice as likely to be unemployed as older white men. (BLS)”

Clearly, there is a concentration of poverty among elders, especially women; and even worse off are people of color who are older in age. Trying to get a job at the “advanced old age” of 62 (early retirement age) or older is difficult. There is no good reason the United States has to leave their elderly in this situation. Nevertheless, it continues because lawmakers claim that the cost for providing seniors with the care they need and deserve would just cost too much. Yet they are content paying for wars, prisons, and tax cuts for the wealthy. The elderly are left to fend largely for themselves or die trying. This we must change.